Getting a health insurance claim denied can feel overwhelming. You pay your premiums, expect coverage, and then face rejection when you need help most. For many people, this is confusing and stressful. That’s where a denied health insurance claim lawyer can make a real difference. They help you fight unfair denials, understand your rights, and get the coverage you deserve. In this article, you’ll learn how these lawyers work, when to hire one, and what to expect from the process. We’ll use simple language, real examples, and practical advice so you can make confident decisions if your health insurance claim is denied.

Why Health Insurance Claims Get Denied

Health insurance companies deny claims for many reasons. Some are valid, but others are mistakes or even unfair tactics. Understanding the common causes helps you know when to challenge a denial.

- Incomplete paperwork – Missing details, wrong codes, or unsigned forms can trigger denial.

- Pre-existing condition – Some plans exclude certain conditions, especially if you had them before buying insurance.

- Out-of-network provider – If you saw a doctor outside your plan’s network, the company may refuse payment.

- Not medically necessary – Insurers often argue that treatment isn’t needed, even when doctors disagree.

- Expired coverage – Claims filed after your policy ends are usually denied.

- Limit reached – Policies often cap how much they’ll pay per year or per illness.

- Mistakes by insurance – Sometimes, denials are simply errors. These can be fixed if you catch them.

Insurers rely on strict rules and complex terms. Even small mistakes can lead to denial. It’s important to read your policy and keep good records. But sometimes, even careful people face unfair rejections.

The Role Of A Denied Health Insurance Claim Lawyer

A denied health insurance claim lawyer is a specialist who fights for your rights when a claim is rejected. They know insurance laws, policy language, and how companies operate. Their job is to help you get the coverage you paid for.

What Lawyers Do

- Review your policy – They check what your insurance promises and what it excludes.

- Analyze denial letters – Lawyers spot weak arguments, missing evidence, or misapplied rules.

- Gather evidence – Medical records, doctor notes, and bills are collected to support your case.

- Write appeals – Lawyers draft strong appeal letters, using legal language that gets attention.

- Negotiate with insurers – Sometimes, lawyers can resolve issues by talking to the company directly.

- File lawsuits – If appeals fail, your lawyer can take the company to court.

Example: Wrongful Denial

Imagine you need surgery. Your doctor says it’s urgent, but the insurer claims it’s “not medically necessary. ” A denied health insurance claim lawyer can show medical proof, challenge the company’s logic, and push for approval. In many cases, appeals succeed if handled correctly.

When To Hire A Denied Health Insurance Claim Lawyer

Not every denial needs a lawyer. Sometimes, simple errors can be fixed by calling the insurance company. But certain situations call for professional help.

Signs You Need A Lawyer

- Large claim amount – If your denied claim is expensive (like surgery or long-term treatment), legal help is wise.

- Complex medical issues – Rare diseases or unusual treatments are often misunderstood by insurers.

- Repeated denials – If you’ve tried to appeal and still get rejected, a lawyer can break the cycle.

- Policy confusion – Insurance documents are hard to read. Lawyers understand them and spot hidden rights.

- Bad faith denial – If the company seems to deny claims without reason, it may be acting illegally.

Practical Tip

Before hiring a lawyer, try contacting your insurer. Sometimes, a simple call clears up confusion. But if you feel lost, pressured, or ignored, get legal advice quickly. Waiting too long can hurt your case.

How The Appeals Process Works

If your claim is denied, you have the right to appeal. This is your chance to show why you deserve coverage. The process follows clear steps, but can be tricky without guidance.

Steps In An Appeal

- Read the denial letter – It explains why your claim was rejected and how to appeal.

- Collect documents – Get medical records, bills, and letters from your doctor.

- Write your appeal – Explain why the denial is wrong. Use facts, not feelings.

- Send everything on time – Appeals have deadlines. Missing them can end your case.

- Wait for review – Insurers must respond, usually within 30 to 60 days.

Lawyer’s Advantage

A denied health insurance claim lawyer knows how to build strong appeals. They use legal arguments, cite policy rules, and add supporting evidence. Many appeals win simply because they are well-prepared.

Real Data

According to the Kaiser Family Foundation, nearly 20% of people who appeal denied claims receive approval. Appeals led by lawyers often have even higher success rates.

Comparing Lawyer Vs. Self-representation

Is hiring a lawyer worth it? Let’s look at the differences between handling a denied claim yourself and using professional help.

| Factor | Self-Representation | Lawyer Representation |

|---|---|---|

| Success Rate | Low to Moderate | High |

| Time Required | High | Moderate |

| Stress Level | High | Low |

| Understanding of Policy | Limited | Expert |

| Cost | Low | Moderate to High |

Lawyers charge fees, but their expertise often leads to better results. For large claims, the investment can pay off.

How Lawyers Charge For Denied Health Insurance Claims

Cost is a big concern. Lawyers use different fee structures depending on your case.

Common Fee Types

- Contingency fee – You pay only if you win. Usually 20-40% of the recovered amount.

- Hourly rate – Some lawyers charge by the hour, typically $150–$400.

- Flat fee – For simple appeals, a lawyer may offer a fixed price.

Example Fee Comparison

| Claim Amount | Contingency Fee (30%) | Hourly Fee (10 hours at $200) | Flat Fee |

|---|---|---|---|

| $10,000 | $3,000 | $2,000 | $1,500 |

| $50,000 | $15,000 | $2,000 | $2,000 |

Contingency fees are common for big claims. For smaller or simpler cases, hourly or flat rates may save money.

Practical Insight

Ask your lawyer about fees upfront. Many offer free consultations. Get everything in writing so you’re not surprised later.

What Makes A Good Denied Health Insurance Claim Lawyer

Finding the right lawyer matters. Not all lawyers have experience with insurance claims. Here’s what to look for:

- Specialization – Choose someone who focuses on health insurance claim denials.

- Track record – Ask about their success rate and previous cases.

- Communication – Good lawyers explain things simply and keep you updated.

- Transparent fees – You should know costs before starting.

- Client reviews – Look for positive feedback from real clients.

Non-obvious Insight

Some lawyers have medical backgrounds or work closely with medical consultants. This helps them understand complex cases and build stronger appeals.

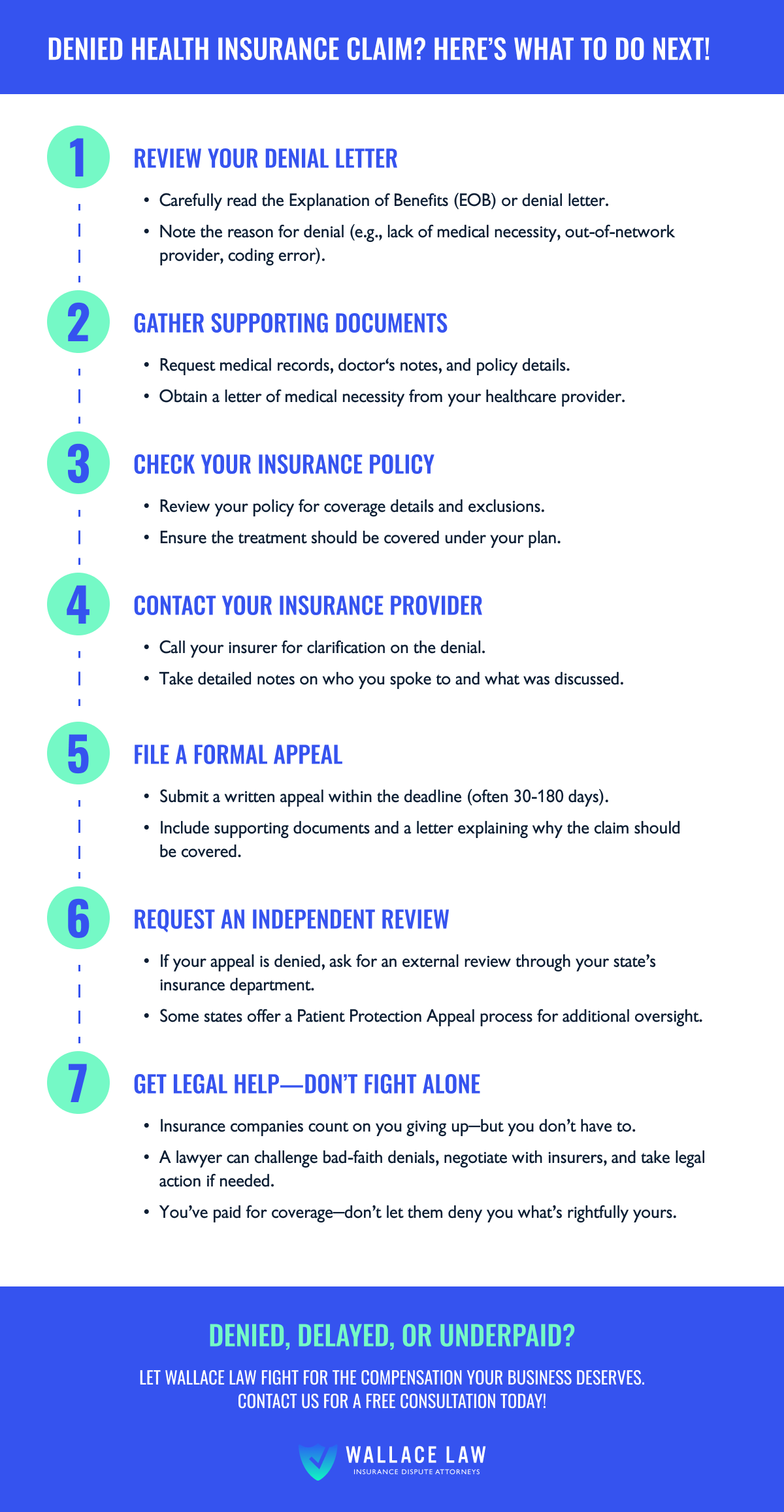

Steps To Take After A Claim Denial

If your claim is denied, act quickly. Delays can limit your options. Here’s a guide for what to do next:

- Read the denial letter carefully. Understand why you were rejected.

- Check your policy for coverage details and rules.

- Call your insurer to ask for clarification. Sometimes, mistakes can be fixed easily.

- Collect all documents – bills, medical records, doctor’s letters.

- Write down deadlines for appeals.

- Contact a denied health insurance claim lawyer if you feel overwhelmed or your claim is large.

Example Mistake To Avoid

Many people ignore denial letters or miss appeal deadlines. Insurance companies count on this. Always act quickly and keep copies of everything you send.

Key Laws Protecting Your Rights

Health insurance in the US is regulated by several laws. Knowing your rights helps you fight unfair denials.

- Affordable Care Act (ACA) – Requires insurers to explain denials and offer appeals.

- Employee Retirement Income Security Act (ERISA) – Covers employer-sponsored plans, giving you the right to sue for wrongful denials.

- State laws – Each state has its own insurance rules. Some offer extra protections.

Useful External Resource

For detailed information on insurance laws, visit the HealthCare.gov Appeals Guide. It explains your rights and the appeal process step by step.

Real-world Example: Successful Claim Appeal

A woman in Texas was denied coverage for cancer treatment. The insurer said it was “experimental. ” She hired a denied health insurance claim lawyer, who found studies showing the treatment was standard. The lawyer wrote a detailed appeal, included medical evidence, and cited the ACA.

The insurer reversed its decision, saving her over $100,000 in medical bills.

Non-obvious Insight

In many cases, insurers rely on vague terms like “experimental” or “not medically necessary. ” Lawyers can use medical research and expert opinions to challenge these claims.

Frequently Asked Questions

What Does A Denied Health Insurance Claim Lawyer Do?

They review your policy, gather evidence, write appeals, negotiate with insurers, and file lawsuits if needed. Their goal is to overturn unfair denials and get you the coverage you deserve.

How Much Does It Cost To Hire A Denied Health Insurance Claim Lawyer?

Costs vary. Many work on contingency, so you pay only if you win. Others charge hourly or flat fees. Ask about fees before starting your case.

How Long Does The Appeals Process Take?

Most appeals take 30 to 60 days. Complex cases or lawsuits can take months or longer. Acting quickly and hiring a lawyer can speed things up.

Can I Appeal A Denial Without A Lawyer?

Yes, but lawyers have more experience and higher success rates. For small claims, you can try yourself. For large or complex cases, legal help is wise.

What Are Common Mistakes People Make After A Claim Denial?

People often ignore denial letters, miss appeal deadlines, or send weak appeals without evidence. Acting quickly and getting help improves your chances.

Facing a denied health insurance claim is tough, but you have options. Lawyers specializing in denied claims give you a real chance to fight back. With the right help, you can get the coverage you deserve and protect your health and finances.

If you’re unsure, don’t wait—get advice and take action. Your health and your rights matter.

Read More:

- Short Term Health Insurance Plans: Fast, Flexible Coverage Options

- Private Medical Insurance UK: Top Benefits and How to Choose

- Compare Family Health Insurance Plans: Find the Best Coverage

- Affordable Health Insurance Quotes: Save Big on Coverage Today

- Best Private Health Insurance Plans: Top Choices for 2024

- Medicare Dental And Vision Coverage: What You Need to Know

- Medicare Supplement Plans Comparison: Find the Best Coverage

- Medicare Prescription Drug Plans: Save Big on Your Medications