Choosing the right Medicare Supplement Plan can feel overwhelming. Many seniors and retirees face confusing choices when their Medicare coverage starts. Original Medicare pays for much, but it does not cover everything. Out-of-pocket costs like deductibles, coinsurance, and copayments can quickly add up. This is where Medicare Supplement Plans—also called Medigap—come in.

Medigap plans help cover these extra costs. They are sold by private insurance companies, but the benefits are standardized by the government. This means that Plan G from one company will offer the same basic coverage as Plan G from another, but prices and service may differ.

Understanding the differences between plans, costs, and what matters most can help you make a smart decision. This article compares the main Medicare Supplement Plans, explains how to choose, and shares key insights for beginners.

What Are Medicare Supplement Plans?

Medicare Supplement Plans are insurance policies that help pay for healthcare costs not fully covered by Original Medicare (Part A and Part B). These plans:

- Cover costs like deductibles, coinsurance, and copayments

- Do not cover prescription drugs (Medicare Part D is needed for that)

- Are available to people aged 65 or older and enrolled in Medicare Part A and B

Medigap plans are labeled by letters: A, B, C, D, F, G, K, L, M, and N. Each plan offers a different set of benefits. Not all plans are available in every state, and some (like Plan F and C) are only open to people who were eligible for Medicare before January 1, 2020.

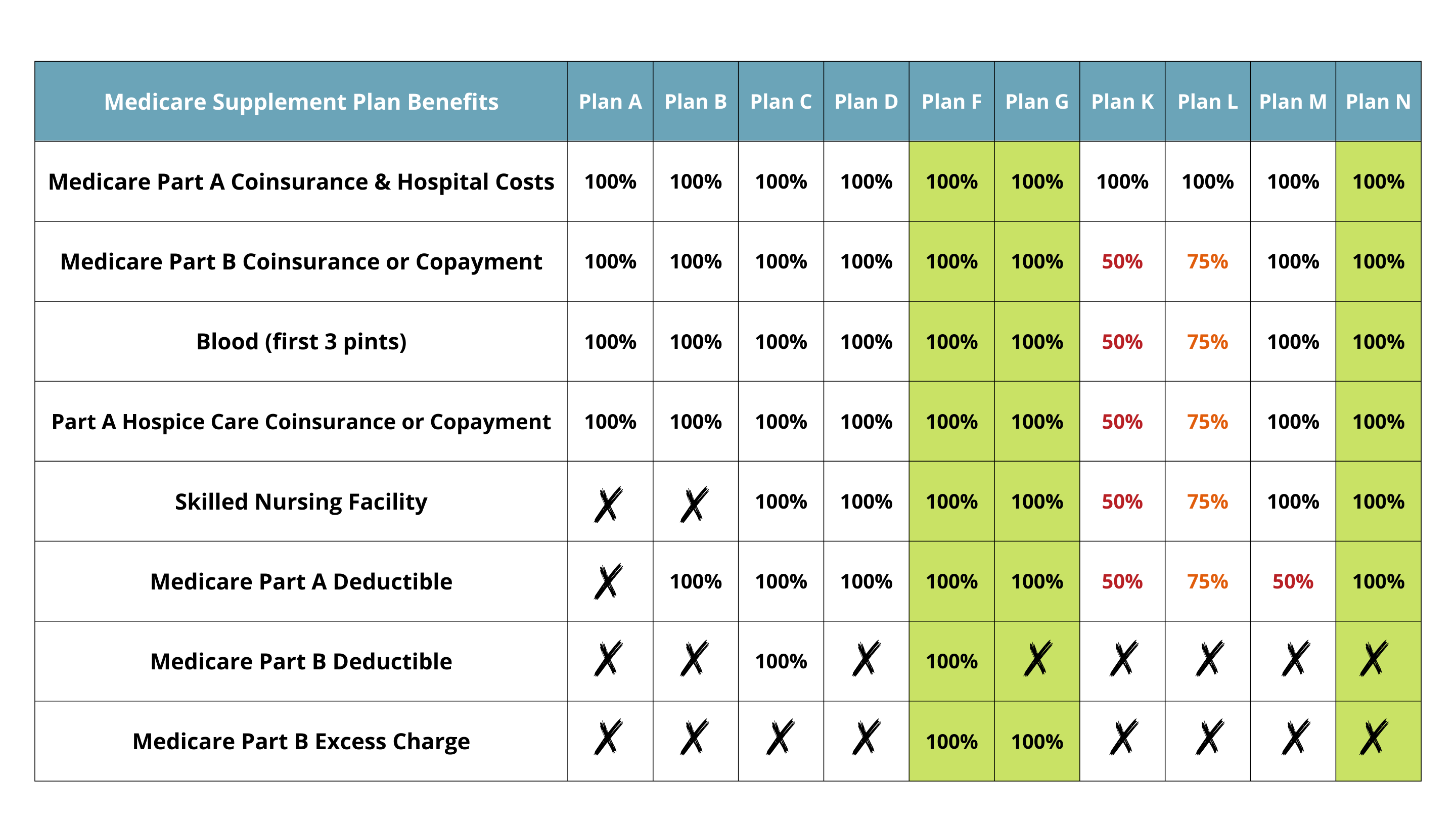

Medigap Plan Comparison

The best way to understand Medigap is to see how the plans compare. Below is a simple table showing which plans cover which costs.

| Benefit | Plan A | Plan G | Plan N | Plan F | Plan K |

|---|---|---|---|---|---|

| Medicare Part A Coinsurance & Hospital Costs | Yes | Yes | Yes | Yes | Yes (50%) |

| Medicare Part B Coinsurance | Yes | Yes | Yes (copay applies) | Yes | Yes (50%) |

| Blood (first 3 pints) | Yes | Yes | Yes | Yes | Yes (50%) |

| Part A Hospice Care Coinsurance | Yes | Yes | Yes | Yes | Yes (50%) |

| Skilled Nursing Facility Coinsurance | No | Yes | Yes | Yes | Yes (50%) |

| Part A Deductible | No | Yes | Yes | Yes | Yes (50%) |

| Part B Deductible | No | No | No | Yes | No |

| Excess Charges | No | Yes | No | Yes | No |

| Foreign Travel Emergency | No | Yes (80%) | Yes (80%) | Yes (80%) | No |

Key Differences

- Plan G covers almost everything except the Part B deductible.

- Plan N covers most costs but has copays for doctor and emergency visits.

- Plan F offers the most complete coverage, but only for people who became eligible for Medicare before 2020.

- Plan K has lower premiums but only covers 50% of most costs. It also has an out-of-pocket maximum.

- Plan A is the most basic, covering only core hospital and medical costs.

Costs And Premiums

Medigap premiums are set by private insurers. The price can vary a lot depending on:

- Your age

- Where you live

- When you buy the policy

- The company you choose

On average, Plan G premiums range from $120 to $180 per month for a 65-year-old. Plan N is often $90 to $140 per month. Plan F is slightly more expensive, around $150 to $200 per month, but is closed to new applicants.

Some plans (like K and L) have lower premiums, but you pay more when you use medical services. The plan’s out-of-pocket maximum is important if you have high health costs.

Here is a sample comparison of premium costs in three states for a 65-year-old:

| State | Plan G | Plan N | Plan K |

|---|---|---|---|

| California | $162 | $129 | $85 |

| Florida | $179 | $145 | $92 |

| Texas | $138 | $114 | $73 |

Premiums are not fixed for life. They can increase over time due to age or company policy changes. This is one reason to review your plan and shop around regularly.

What To Consider When Comparing Plans

Choosing the right Medigap plan is not just about picking the cheapest premium. Here are important factors to compare:

1. Coverage Needs

If you often visit doctors, a plan with fewer copays (like Plan G) may save money. If you are healthy and rarely need care, a lower premium plan like Plan K or N may be enough.

2. Budget

Some plans have higher monthly costs but lower out-of-pocket costs. Others are cheaper monthly but require you to pay more when you use services.

3. Provider Flexibility

Medigap lets you see any doctor who accepts Medicare. This is a big advantage over some Medicare Advantage plans, which use networks.

4. Out-of-pocket Maximum

Plans K and L have yearly limits on how much you pay. Other plans do not.

5. Foreign Travel Coverage

Only some plans cover emergency care outside the US. If you travel, check for this feature.

6. Company Reputation

Prices can be similar, but service quality varies. Look for companies with strong customer reviews and financial stability.

7. Plan Availability

Not all plans are offered in every state. Some states (like Massachusetts, Minnesota, Wisconsin) use different rules.

Common Mistakes When Choosing Medigap

Many beginners make these errors:

- Not comparing enough companies. Premiums for the same plan can vary by hundreds of dollars.

- Ignoring future health needs. Picking the cheapest plan may cost more later if your health changes.

- Waiting too long to enroll. The best time to buy is during your Medigap Open Enrollment Period—the 6 months after you turn 65 and enroll in Medicare Part B. After that, you may have to answer health questions and pay higher premiums.

- Confusing Medigap with Medicare Advantage. Medigap supplements Original Medicare. Medicare Advantage replaces it and has different rules.

Popular Medigap Plans Explained

Let’s look closer at the most popular plans.

Plan G

- Covers almost all gaps except the Part B deductible ($240 in 2024)

- Includes skilled nursing, foreign travel, and excess charges

- Suitable for those wanting strong coverage but not eligible for Plan F

Plan N

- Lower premiums than G

- Copays: Up to $20 for doctor visits, up to $50 for ER (if not admitted)

- Does not cover excess charges (some doctors may bill extra)

- Good for people who don’t visit doctors often

Plan F

- Covers everything, including Part B deductible

- Only available if you were eligible for Medicare before 2020

- Highest premiums, but least out-of-pocket costs

Plan K

- Lowest premiums

- Pays 50% of most cost-sharing except hospice and hospital coinsurance

- Annual out-of-pocket limit ($6,620 in 2024)

- Useful if you want a safety net but can handle some costs

Comparing Medigap Vs. Medicare Advantage

Some people confuse Medigap with Medicare Advantage. They are very different.

| Feature | Medigap | Medicare Advantage |

|---|---|---|

| Provider Choice | Any Medicare provider | Usually network only |

| Prescription Drugs | Not included | Often included |

| Coverage Area | Nationwide | Local |

| Plan Structure | Standardized | Varies |

| Extra Benefits | No extras | May offer vision, dental, etc. |

| Out-of-Pocket Maximum | Only some plans | Yes |

If you want flexibility and nationwide coverage, Medigap is often the better choice. If you want lower premiums and extra benefits, Medicare Advantage can be attractive, but check network restrictions.

Two Insights Beginners Often Miss

1. Premiums Can Change Annually

Many people think their Medigap premium will stay the same. In reality, companies can raise rates due to age or other factors. It’s wise to review your plan every year.

2. Excess Charges Matter

Plans G and F cover “excess charges”—extra fees some doctors charge above Medicare’s approved amount. If you live in a state where doctors often bill these charges, picking a plan that covers them can prevent surprise bills.

How To Shop For Medicare Supplement Plans

- Compare at least 3–5 companies in your area.

- Check the plan’s benefits, not just the price.

- Ask about rate increases over time.

- Read customer reviews and ask friends or family for recommendations.

- Use official resources like Medicare.gov to find plans and prices.

Frequently Asked Questions

What Is The Best Medicare Supplement Plan?

There is no single “best” plan for everyone. Plan G is popular because it covers most costs, but your health needs and budget may make another plan better.

When Can I Buy A Medigap Plan?

The best time is during your Medigap Open Enrollment Period—the 6 months after you turn 65 and enroll in Medicare Part B. After that, you may have to answer health questions and pay more.

Are Medigap Premiums Tax-deductible?

If you itemize deductions, some or all of your premiums may be tax-deductible as medical expenses. Always check with a tax advisor for your situation.

Do Medigap Plans Cover Dental Or Vision?

No. Medigap covers only medical costs that Original Medicare does not. For dental or vision, you need separate insurance.

Can I Switch Medigap Plans Later?

Yes, but after your first enrollment period, you may face health questions and higher premiums. It’s easier to switch within your first 6 months.

Choosing a Medicare Supplement Plan is a big step for your health and finances. Take your time, compare carefully, and ask questions. The right plan can give peace of mind and save money in the long run.

Read More:

- Short Term Health Insurance Plans: Fast, Flexible Coverage Options

- Private Medical Insurance UK: Top Benefits and How to Choose

- Compare Family Health Insurance Plans: Find the Best Coverage

- Affordable Health Insurance Quotes: Save Big on Coverage Today

- Best Private Health Insurance Plans: Top Choices for 2024

- Medicare Dental And Vision Coverage: What You Need to Know

- Medicare Prescription Drug Plans: Save Big on Your Medications

- Best Medicare Advantage Plans: Top Picks for 2024 Coverage